How to Maximize the QBI Deduction Amid the Pandemic

Since the qualified business income (QBI) deduction first become available in 2018, things have changed dramatically, mainly due to the various effects of the COVID-19 pandemic. Possible tax rate increases and inflation have also entered into the mix. How do these developments affect planning to maximize QBI deductions for your business?

The Basics

The QBI deduction was one of the cornerstones of the Tax Cuts and Jobs Act. For 2018 through 2025, the deduction is available to eligible individuals, trusts and estates, but it's not available to C corporations or their shareholders.

The QBI deduction can be up to 20% of:

What's a SSTB?

In general, a specified service trade or business (SSTB) means any trade or business involving the performance of services in one or more of the following fields:

Health, law, accounting, and actuarial science (architecture and engineering firms aren't considered SSTBs),

Consulting,

Financial, brokerage, investing and investment management services,

Trading,

Dealing in securities, partnership interests or commodities,

Athletics and performing arts, and

Any trade or business where the principal asset is the reputation or skill of one or more of its employees or owners.

Before the IRS issued regulations, there was concern that the last item on this list could snare unsuspecting businesses, including local restaurants with well-known chefs. Thankfully, the regulations limit the last definition to trades or businesses that receives fees, compensation, or other income for:

An individual endorsing products or services,

The use of an individual's image, likeness, name, signature, voice, trademark or any other symbol associated with that person's identity, and

An individual's appearance at an event or on radio, television or other media platform.

QBI earned from a sole proprietorship or single-member limited liability company (LLC) that's treated as a sole proprietorship for federal income tax purposes, plus

QBI from a pass-through business entity, meaning a partnership, LLC classified as a partnership for federal income tax purposes or an S corporation.

Pass-through business entities report their tax items to their owners who then take them into account on their owner-level returns. The QBI deduction, when allowed, is then written off at the owner level.

Important: This article focuses on individual taxpayers who can claim QBI deductions, with the understanding that essentially the same considerations apply to trusts and estates.

Close-Up on QBI

QBI means qualified income and gains from an eligible business reduced by related deductions and losses. QBI from a business is reduced by allocable deductions for:

Contributions to a self-employed retirement plan,

Part of your self-employment tax bill, and

Self-employed health insurance premiums.

The following items do not count as QBI:

Income from the business of being an employee,

Guaranteed payments received by a partner or an LLC member treated as a partner for tax purposes for services rendered to the business,

Salary collected by an S corporation shareholder-employee, and

Salary collected by a C corporation shareholder-employee.

On your personal return, the QBI deduction doesn't reduce your adjusted gross income (AGI). In effect, it's treated the same as an allowable itemized deduction.

Unfortunately, the QBI deduction doesn't reduce your net earnings from self-employment for purposes of the self-employment tax nor does it reduce your net investment income for purposes of the 3.8% net investment income tax (NIIT) on higher-income taxpayers.

Limitations

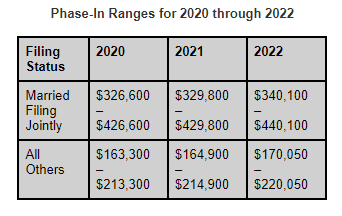

At higher income levels, unfavorable QBI deduction limitations may come into play. These income limits are indexed annually for inflation. Here are the income-based phase-in thresholds for 2020 through 2022:

These limitations are phased in over a taxable income range of $50,000, or $100,000 for married couples who file joint returns.

If you exceed the applicable fully phased-in threshold, your QBI deduction is limited to the greater of:

Your share of 50% of W-2 wages paid to employees during the tax year and properly allocable to QBI, or

The sum of your share of 25% of such W-2 wages plus your share of 2.5% of the unadjusted basis immediately upon acquisition (UBIA) of qualified property.

The limitation based on the UBIA of qualified property is for the benefit of capital-intensive businesses, such as manufacturing or hotel operations. Qualified property means depreciable tangible property (including real estate) that meets the three criteria:

It's owned by a qualified business as of its tax year end,

It's used by that business at any point during the tax year for the production of QBI, and

It hadn't reached the end of its depreciable life as of the tax year end.

The UBIA of qualified property generally equals its original cost when it was first put to use in your business.

Finally, your QBI deduction can't exceed 20% of your taxable income calculated before any QBI deduction and before any net capital gain (net long-term capital gains in excess of net short-term capital losses plus qualified dividends).

Unfavorable Rules for SSTBs

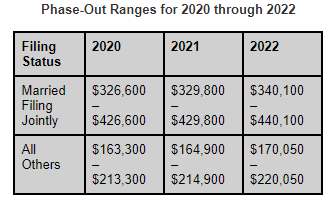

If your operation is a specified service trade or business (SSTB), QBI deductions begin to be phased out when your taxable income (calculated before any QBI deduction) exceeds the applicable threshold. See "What's a SSTB?" above.

The following phase-out ranges apply to SSTBs for 2020 through 2022:

If your taxable income exceeds the top of the applicable phase-out range, you're not allowed to claim any QBI deduction based on income from any SSTB.

Effects of Income Reductions

Many businesses had lower income in 2020 and 2021 — and they may also have lower income this year. However, the impact on your allowable QBI deduction could go either way. Other things being equal, lower income translates into lower QBI deductions. But lower income can also mitigate the impact of the unfavorable QBI deduction limitations. This can be confusing, but your tax advisor can clarify your situation.

QBI Deduction Planning Moves

Remember that, as the law reads now, the QBI deduction is scheduled to disappear after 2025. So, it's essentially a use-it-or-lose-it deal. Congress could extend this deduction, but you probably shouldn't bet on that happening. Here are three possible strategies for you to consider to help maximize QBI deductions through 2025.

1. Aggregate businesses. Aggregating businesses can allow an individual with taxable income high enough to be affected by the limitations (based on W-2 wages and the UBIA of qualified property) to claim a bigger QBI deduction than if the businesses were separate.

For instance, say you're a high-income individual who owns an interest in one business with significant QBI but little or no W-2 wages and an interest in a second business with minimal QBI but significant W-2 wages. Aggregating the two businesses can result in a healthy QBI deduction, while keeping them separate could result in a lower deduction or maybe none at all. However, tests set forth in IRS regulations must be passed for you to be allowed to aggregate businesses.

Important: You can't aggregate a SSTB with any other business, including another SSTB.

2. Claim (or forego) first-year depreciation deductions. Under current tax law, you can claim 100% first-year depreciation deductions and/or big first-year Section 179 depreciation deductions for most business assets that are placed in service through the end of 2022.

First-year depreciation deductions reduce your QBI — but they also reduce taxable income, which could reduce the impact of the unfavorable QBI limitations. All things being equal, lower taxable income is generally desirable. So, you may have to tread a fine line with depreciation write-offs to get the best overall federal income tax result.

Important: The QBI deduction may be a use-it-or-lose it deal. In contrast, when you forego first-year depreciation deductions, you can still depreciate the assets over a number of years under the "regular" depreciation rules. If tax rates go up, depreciation deductions claimed in future years could turn out to be worth more than sizable first-year depreciation deductions claimed in earlier years.

3. Make (or forego) large deductible retirement plan contributions. Deductible self-employed retirement plan contributions allocable to a business that generates QBI will reduce your allowable QBI deduction — but they also reduce your taxable income, which could reduce the impact of unfavorable QBI limitations. Again, all things being equal, lower taxable income is generally desirable. So you may have to tread a fine line with retirement plan contributions to get the best overall federal income tax result.

Impact on Prior Returns

If you've not yet filed your 2021 Form 1040 that includes income and deductions from a sole proprietorship or pass-through entity business that could generate a QBI deduction, consider the ideas above before filing.

Similarly, you may be able to file amended 2020 returns that take some of these ideas into account. Consult your tax advisor.

It's Complicated

The QBI deduction rules are lengthy and complex. Your tax professional can sort through the details and determine how to get the optimal federal income tax results for your situation.